Providing liquidity on Stargate Omnichain

Key Takeaways:

- This strategy fits the profile of an investor who is willing to take on increased risk in exchange for a greater reward.

- The protocol is rather new, only going live in March 2022. The newer the protocol, the higher the risk that vulnerabilities exist which have not yet been spotted and/or exploited (tech risk).

- Stargate is a cross-chain bridge protocol enabling the transfer of native assets between different blockchain networks. Simply speaking it allows users with, as an example, BUSD on Binance chain to transfer the asset to the Avalanche network and to cross swap it into USDT. For this to work, a fundamental underlying assumption is that the value of any given stablecoin is strictly equal across chains, as in, 1 BUSD on Binance equals 1 USDT on Avalanche.

- While the strategy is fairly simple, it involves up to 1 chain (BNB), 1 stablecoin (BUSD), and two types of transactions: 1) a deposit into the pool, and 2) a transfer of the received Liquidity Provider (LP) tokens to the farming pool. Imbalances in the pools are caused by investors transferring tokens between chains may affect the ability for a user to redeem deposits (liquidity risk).

- The Yield (APY) is composed of:

- exchange fees,

- farming rewards. - Because the LP tokens are farmed, an additional smart contract is employed, subjecting investors to a second potential vulnerability (tech risk).

- Most of the Annual Percentage Yield (APY) comes from farming rewards. These rewards are subsidised by the protocol and may not be fully sustainable in the future (yield sustainability risk). Nevertheless, the strategy offers daily liquidity without the constraints of a lockup. For this reason, investors will be able to quickly adjust to any changes of market conditions.

- Risk Checklist

In our view the predominant risks for this strategy are as follows:

- Tech Risk

- Liquidity Risk

- Sustainability Risk

1. Strategy Explained

The strategy is fairly simple; provide liquidity into a Stargate Finance BUSD pool on the BNB chain and farm the liquidity provider (LP) tokens.

Stargate is a cross-chain bridge protocol that enables the transfers of native assets between different blockchain networks. Simply put, it allows users, with let’s say BUSD on Binance chain, to transfer it to USDT on Avalanche. This swap is facilitated by having two pools, one BUSD pool on Binance and one USDT Avalanche. The user deposits BUSD in the Binance pool and immediately receives the same amount in USDT – minus fees – from the Avalanche pool.

Pool liquidity exists thanks to liquidity providers who deposit BUSD and USDT into the pools and gain a 4.5 basis point fee, 0.045%, on all transactions.

In addition to transfer fees, LP tokens – which are a sort of certificate of ownership for the deposited BUSD – can be farmed within the protocol to gain additional rewards in the Stargate protocol native token STG.

Lockup period: None. Assets can be redeemed at any time.

2. Strategy Risks

Stargate Finance Tech Trust Score

With a total-value-locked (TVL) of over $500 million, Stargate is the largest cross-chain protocol in DeFi. The protocol went live in March 2022 attracting an astonishing $1.6 billion of TVL in just 6 days of operation, and so far has not been subject to any exploits or hacks.

The SwissBorg Tech Trust Score for Stargate Finance is ‘green’ meaning the protocol is trustworthy.

The score is 70%, signalling that the protocol represents a relatively safe choice.

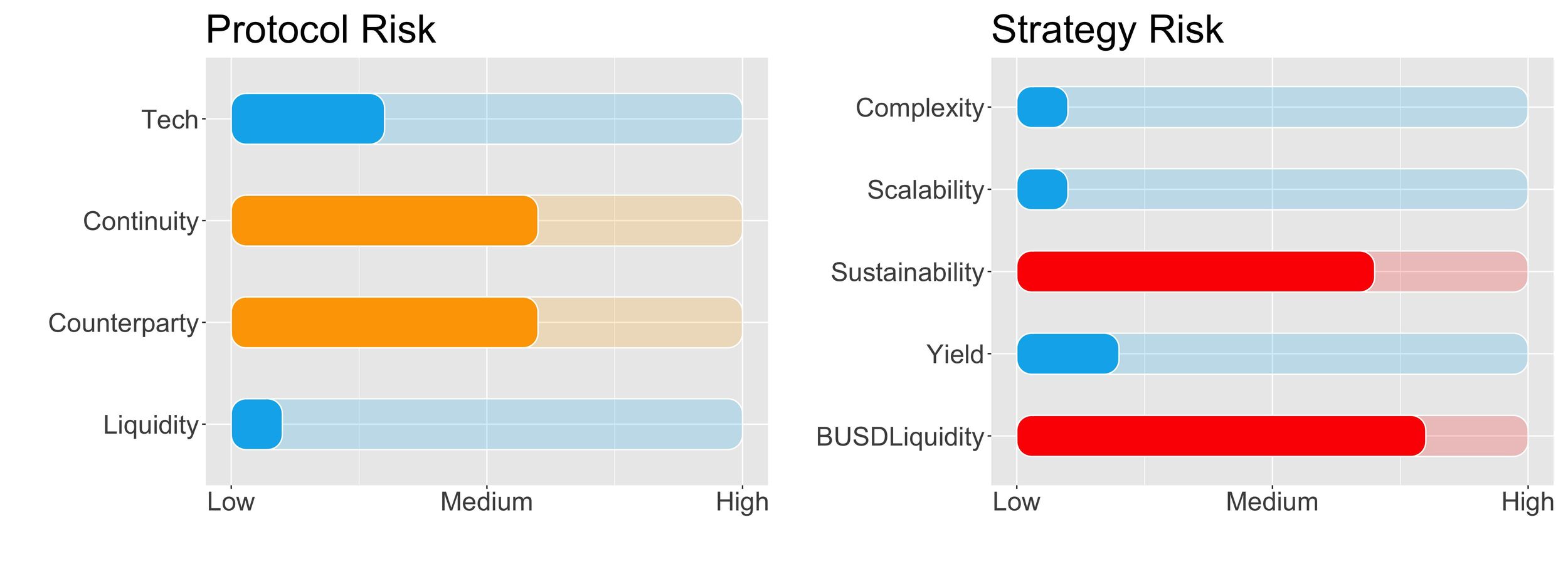

Protocol Risk

Project Continuity Risk

The risk associated with the continuity of the Stargate project is ranked as medium.

Stargate Finance displays the largest TVL among competing cross-chain protocols, but lags behind when compared to top DeFi protocols like the lending platform AAVE, or the Decentralised Exchange (DEX) Uniswap.

In terms of valuation, the token’s TVL ratio – a calculation of its market capitalization over its TVL – is 0.09. A protocol with a TVL ratio below 1 can be considered undervalued, this idea further supported by the fact that it ranks higher than most other cross-chain protocols in other ways.

The final point on protocol risk, no market sentiment score could be computed from LunarCrush’s GalaxyScore since the protocol is not yet covered. The Galaxy Score is a combined measure of cryptocurrency indicators used to correlate and understand the overall health, quality and performance of a specific project. In short, it indicates how well a coin is doing. As the Stargate project is quite young, no coverage from LunarCrush exists. This also means that it is not ‘battle tested’, never having gone through a full crisis period or bear market.

This conservatively triggers a medium to high risk rating in terms of market sentiment.

Project Continuity Risk is 6/10.

Counterparty Risk

Overall counterparty credit risk for Stargate is considered medium.

Stargate protocol offers simple transfer of tokens from protocol A to protocol B, instantaneously. With this capability, borrowing activity can be performed, meaning there should be no risk that the protocol becomes insolvent.

There is however a situation where users could lose part of their funds. This condition would be if pools are imbalanced and one stablecoin loses its peg. For example, let’s assume an investor deposits $1 million into the Ethereum USDC pool. Due to market events, participants are worried about the peg of USDT. They start swapping USDT for USDC within Ethereum, but also across chains. This means they will deposit USDT in the Avalanche pool, for example, and receive USDC from the Ethereum pool. This process will create an imbalance of USDT vs. USDC.

Let’s now assume USDT eventually loses its peg. The investor is left with a USDC position but the majority of assets in the protocol are in USDT. Because it is now depegged, the value of the USDT does not cover the initial USDC deposits – additionally, there could be insufficient liquidity in USDC to satisfy a redemption, as per the Liquidity Risk defined below. In such a situation the investor is stuck in a protocol which is virtually insolvent, given that liabilities are larger than assets, and unable to exit his position.

Counterparty risk is 6/10.

Liquidity Risk

Overall liquidity risk for Stargate is low.

The protocol is always in a balanced state with respect to the total amount of deposits, since tokens simply move from one pool to another. For this reason, the protocol itself faces virtually no liquidity risk.

Liquidity risk for Stargate is set at 1/10.

Strategy Risk

Complexity

Complexity of the strategy is medium.

The strategy is simple; deposit BUSD into the Stargate Binance pool and receive both:

- a yield as a percentage of every transfer executed using that pool,

- a reward in Stargate’s native token STG for farming the LP tokens – which act as a sort of IOU representing one’s share of the pool.

Although the strategy is not complex and it involves: 1 token, 1 protocol and 1 chain.

Last but not least, because LP tokens are farmed, depositors will need to execute a smart contract to let the LP tokens be farmed. This process involves a higher degree of trust from the depositor as issues with these smart contracts could put deposits in peril.

Complexity of the strategy is rated 1/10.

Scalability

Scalability risk of the strategy is low for BUSD.

At the time of writing, the BUSD pool in Stargate displays a liquidity of $41m. Currently, around $700k in BUSD is in the yield program, leaving room for scaling up in terms of assets under management (AUM).

Scalability risk of the strategy is 1/10.

Sustainability

Sustainability risk of the strategy is medium to high.

Yield on Stargate is derived from collecting trading fees plus farming rewards. Trading fees reflect the supply/demand of transferring tokens between chains and is therefore a fully sustainable yield.

Trading fees alone, however, would be very small, from 2% on Avalanche and close to 0% on Ethereum. Because of this feature, most of the yield comes from actually farming the LP tokens in exchange for Stargate rewards, in the token STG.

With farming, the protocol itself generates yield from investors' deposits. This could be done in multiple ways and at a level of risk that goes beyond the simple collection of trading fees.

Sustainability risk is rated 7/10.

Yield Risk

Yield risk is low.

Yield risk represents the volatility of the expected yield on BUSD. Stargate trading fees are collected as a fixed percentage of transfer volumes at 45 basis points, or 0.045%. Trading volumes are a function of the prevailing market conditions and are dynamic.

In addition, most of the APY is obtained from the farming rewards. While this can pose some issues in terms of future sustainability (see the Sustainability section) they are expected to represent a constant stream of income.

Yield risk is set to 2/10.

LP on cross-chain strategy specific: Liquidity Risk

Liquidity risk for a specific BUSD pool in Stargate is deemed medium to high.

The main risk associated with Stargate Finance is the inability to exit a position; to withdraw the deposits due to a lack of available liquidity.

The main difference between Stargate and a lending protocol is that in the case of an imbalance there are no borrowers being charged high rates. When this happens in lending/borrowing this represents an incentive for a borrower to reduce their exposure and thus increase the available liquidity in the pool. In addition, the increase in liquidity risk is mitigated by higher rates received by the lenders.

In Stargate, in the presence of imbalances, transfer fees are increased, effectively attracting more lenders on the short side. On the one hand, if no transaction happens, lenders are not rewarded with higher rates, but may still face issues when trying to redeem. On the other hand, because rebalancing is only incentivized passively via higher future fess, the speed of adjustment of the pool is expected to be lower.

Nevertheless, in principle a liquidity provider could immediately redeem its deposited tokens even if not available in the original pool. The tokens would be made available in a liquid pool on some other chain. Bridging back the funds to the original chain could be time consuming and costly as, for example, one would need to deposit USDT on the Ethereum chain, but get back part of the funds in USDC on Avalanche. These last tokens would need to be bridged from Avalanche to Ethereum.

In the extreme scenario that there is no liquidity pool across the chains able to satisfy a redemption, the USD amount equivalent to the deposited stablecoin would be available in some other stablecoin. Therefore the liquidity provider would incur additional swapping costs – along with the bridging costs mentioned earlier – to revert back to the initial stablecoin. This process could erode part of the APY because under this extreme scenario, a liquidity provider would deposit USDC on Ethereum, but would only be able to immediately withdraw USDT on Avalanche. This would result in having to perform two operations: swapping USDC for USDT and bridging them over to Ethereum.

Recall that, differently from USDT and USDC, there is only one BUSD pool in Stargate. So if this pool had no sufficient exit liquidity, the investor would have to necessarily exit on a different chain and different coin combinations.

Lastly, there is no straightforward way of checking the pool balance / pool imbalance from the Stargate website. Liquidity can only be monitored by looking at the smart contract address of each pool.

Liquidity risk for BUSD on Stargate is 8/10.

3. Conclusions

Our thoughts on Stargate are mixed.

From the significant investment it has received, the market has clearly accepted it as a viable option as a ‘stablecoin liquidity bridge’ and it has performed without a hitch since going live in March of this year. It is a clever and potentially stable form of income from the movement of stablecoins over networks.

That being said, the structure it is built upon is fragile being highly reliant on the stability of the stablecoins it works with resulting in less control, an issue that has proved fatal for other projects. The idea that a situation could arise where holders would not be able to withdraw their positions due to a lack of liquidity is troubling. Adding to this is the risk associated with the extra operation of farming liquidity pool tokens, subjecting the investor to additional potential IT vulnerability.

The SwissBorg Risk Team ranks Stargate as an Medium risk investment, one for a crypto-fluent, experienced, market-aware investor who fully understands the associated risks.

This investor is willing to take a position and watch it closely, with high risk and elevated rewards. For this investor type, we recommend using a small investment to see and learn how the protocol works as an act of due diligence before making any larger moves.

Disclaimer: This report is intended for general guidance and informational purposes only and does not constitute any offer to the public of virtual assets or financial instruments, financial advice, investment advice, or any other type of advice, and should not be interpreted or understood as any form of promotion, recommendation, solicitation, offer or endorsement to (i) buy or sell any product, (ii) carry out transactions, or (iii) engage in any other legal transaction. Any opinions expressed herein are those of the authors and do not represent the views or opinions of SwissBorg Solutions OÜ and neither of its affiliates. Neither SwissBorg Solutions OÜ nor its affiliates, make any representation or warranty or guarantee as to the completeness, accuracy, timeliness or suitability of any information contained within any part of this report, nor to it being free from error. Recipients alone assume the sole responsibility of evaluating the merits and risks associated with the use of any information contained in this report before making any decision based on such information and should not act upon this information without seeking prior professional advice.

Try the SwissBorg Earn today!

Date modified: