Introducing CeFi and DeFi

There is no argument that the advent of blockchain democratised access to finance. And because of the distributed nature of blockchain, it has become a hotbed for innovation. Especially in finance, newer and interesting solutions pop up, posing both challenges and risks to the legacy financial industry.

The major players in the decentralised ledger technology and cryptocurrency industry can be grouped into two broad categories. These are CeFi and DeFi, or Centralised Finance and Decentralised Finance.

Let’s start by giving simple definitions for these concepts. CeFi mimics the legacy financial industry by allowing people to earn interest or get loans, whereby they use their cryptocurrencies as a form of collateral. In a nutshell, corporations act as lenders and bear custody of their clients’ funds/assets while they put them to use to provide interest for the lenders. The crucial thing to consider here is that lenders transfer risks to these corporations. Notable examples include big exchanges like Binance, Coinbase or even the likes of Celsius, SALT, etc.

DeFi refers to the application of smart contracts to financial instruments thereby removing the need for users to trust a middleman or corporation. DeFi offers a slew of products such as flash loans, derivatives, permissionless trading and margin calls, insurance, etc. With DeFi, users trust a protocol rather than a corporation or human, i.e. they trust codes to deliver on any human or entity’s behalf. Examples include MakerDAO, Compound, dYdX, Uniswap, Balancer, etc. The spate of growth in this section of the industry has seen within the last year has been exponential.

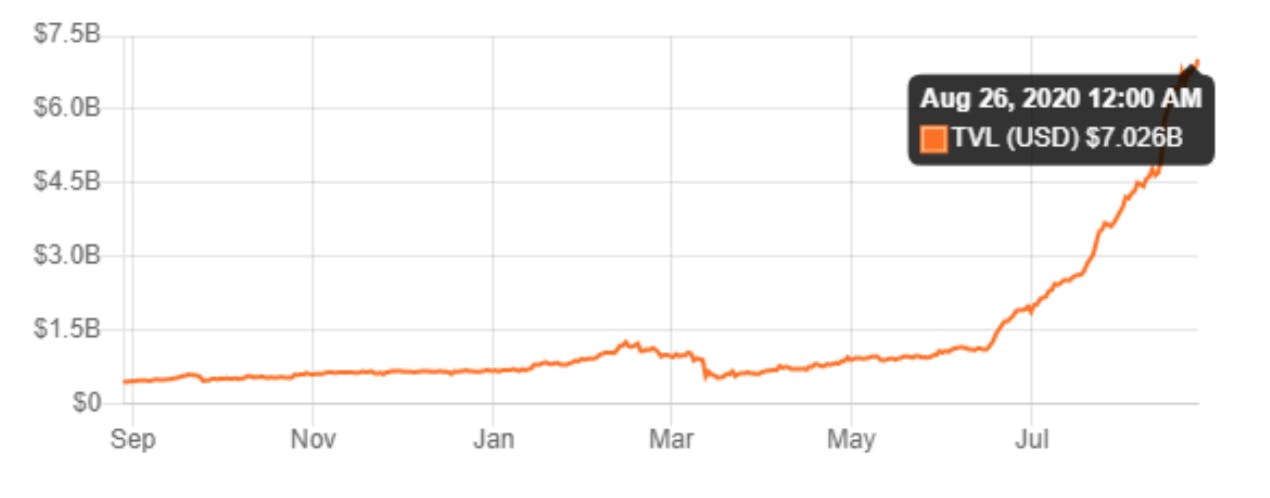

While CeFi platforms have had their run and are still enjoying high patronage within the industry, DeFi has also been growing rapidly. DeFi enthusiasts have locked more than 6 billion USD across several protocols. Maker, Aave, Curve, Compound and a few others lead the pack.

Benefits of DeFi and CeFi

Both approaches come with their unique benefits. For CeFi, one of the most important benefits is risk-transference. Just like legacy banking services, where banks and lending institutions insure depositors funds, CeFi corporations guarantee both safety and returns for their users. The obvious reason here is because they bear custody. While there may not be a hundred percent guarantee as most T&Cs depict, but CeFi users can, at least, rest assured that their funds are in safe custody. Binance, Coinbase and other crypto banks that have been operating for years do everything to make sure user funds are secured. On another note, CeFi platforms usually come with a highly intuitive and easy-to-use interface. Newbies can easily onboard onto these platforms to enjoy their services. The goal is to expose cryptocurrencies to as many people as possible. And CeFi platforms do well in this area.

On the other hand, DeFi comes with the obvious advantage of non-custody. Decentralised protocol users have full control of their funds. They only need to interact with a protocol’s interface to carry out their activities which include, but are not limited to, trading, lending or even swapping from one token to another.

The common drawbacks for CeFi vs DeFi

Although both have their advantages, they also come with their disadvantages. For CeFi, the biggest disadvantage or risk associated with these platforms is custody. Centralised platforms with high liquidity are always a target for hackers. The popular mantra “not your keys, not your coin” is always the first argument of those in favour of complete decentralisation hold out make to victims who may have had their funds compromised in any centralised system.

As for DeFi protocols, as users do not have to trust entities or human beings but code, an inherent flaw in the code may spell a huge disaster. Non-custodial finance also means you are responsible for your risk. While anyone may argue this is a necessary principle for personal finance, newbies who may not know the underlying risks behind a protocol may be burnt in the event of a bug. A good example is the recent YAM protocol failure where users deposited as much as 600 million USD in an unaudited protocol and had to start a panic withdrawal upon the discovery of a fatal bug. Also, many decentralised applications cannot boast of an attractive user interface and experience, UI/UX. Perhaps this is one of the reasons it took so long for the DeFi industry to pick up as we saw recently.

What to expect in DeFi vs CeFi in the future?

As the industry evolves and addresses challenges like hacks, the overall ecosystem will keep improving with time. Both DeFi and CeFi have valid places in the cryptocurrency movement. They offer attractive yields, faster transactions, and infrastructure that promotes more open finance. Both of these visions will improve are key drivers for financial inclusion, which is the overall goal of most financial applications.

So, whether your preference is for DeFi or CeFi, the innovations will almost certainly mean the end of traditional banking as we have come to know it. However you look at it, it’s still a net positive for everyone, especially cryptocurrency enthusiasts.

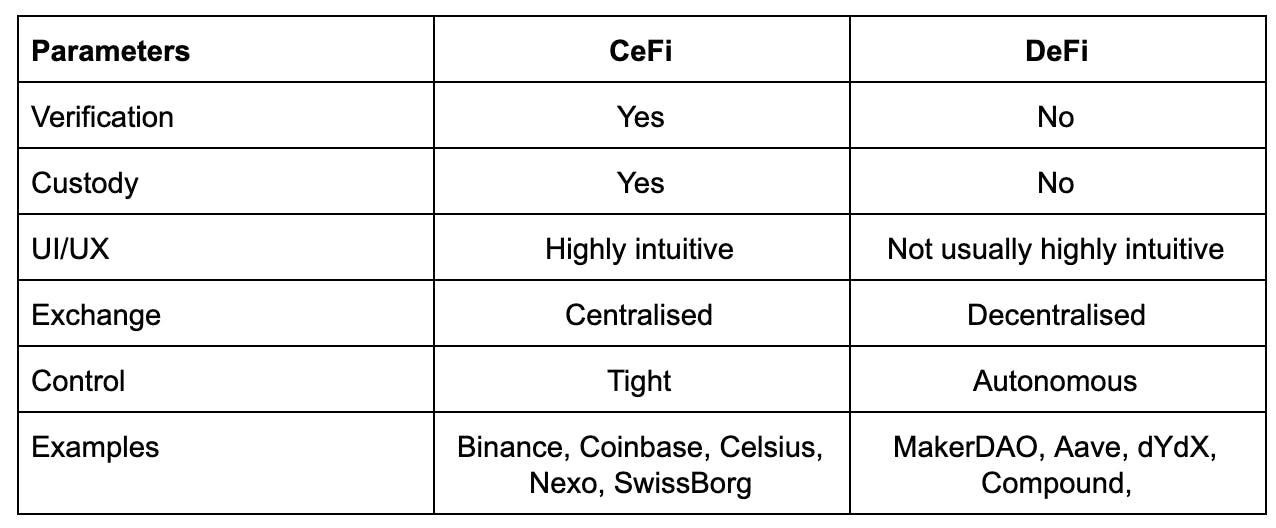

Below is a table that summarises the differences between CeFi vs DeFi:

Where does SwissBorg fit in?

Even though SwissBorg falls in the CeFi category, it can be properly described as a bridge between DeFi and CeFi. One thing we have established in this article is that CeFi is not at all bad from the angle of user experience and ease of use, risk transference and high liquidity.

SwissBorg’s SwissBorg app takes away the stress and inherent risk in remembering and keeping private keys or passphrase safe by opting for the MPC security system . Remember that the best way to keep something safe is to not have the risk exist in the first place. So while traditional CeFi may be vulnerable to hackers because of centralised security systems but possess high liquidity, SwissBorg’s MPC distributed keyless system reduces this risk. This bridges the gap that exists when you compare DeFi’s private key system which is non-custodial but may be prone to misplacement. This technology makes SwissBorg’s Wealth App one of the best and secure crypto wallets in the industry.

Furthermore, talk about liquidity, and SwissBorg aptly comes to mind. Its Wealth App besides being one of the best alternatives to buy Bitcoin within the crypto industry also comes with an array of other coins. Some of them include the highly liquid Binance Coin (BNB), easy access to the industry’s second-largest stablecoin, USDC to easily hedge against volatility and a slew of other coins like Ethereum, Enjin, and Binance Coin. They have also added two new DeFi tokens to the mix - Aave and Kyber - and have a slew of exciting new assets joining soon. Get a list of the SwissBorg Wealth app supported assets .

The app also supports easy crypto to fiat conversion with the cheapest fees in the industry. While many trading apps may like to hide their fees, SwissBorg is transparent with its fees structure. See a comprehensive list of SwissBorg app fees here . It’s also important to mention that even with the DeFi boom and non-custodial nature of some of the DEXes like Uniswap, Curve and Balancer, fees traders have had to pay during this time where the Ethereum network is facing congestion is mind-boggling. SwissBorg’s Wealth app is a timely and credible alternative to the rescue here.